International Montoro Resources Inc. (TSX-V: IMT) /(OTCQB: IMTFF) /(Frankfurt: O4T1) is trading at a very cheap valuation, an Enterprise Value (“EV“) of ~C$4.5M. This is absurd given the Company’s existing assets, near-term prospects & expert deal-making team. In addition to two promising gold properties, IMT has two Nickel-Cu-PGE-Co projects (all in Ontario), and a REE project in B.C.

The Company’s Wicheeda North REE project alone is arguably worth as much or more than IMT’s entire EV. Adjoining this 1,444-hectare property is Defense Minerals’ 1,708-hectare Wicheeda REE project. Defense Metals is a single-project company with a market cap of $8M. I believe IMT’s smaller and less developed REE property is, nonetheless, worth at least $4.5M.

The following four properties are the primary assets being advanced at this time. Note, another acquisition was announced just hours ago! Two high-grade gold properties in Central Newfoundland. I will follow up these properties in my next article.

Wicheeda North, B.C. (REE), Blackfly, Atikokan, Ontario (gold), Serpent River/Pecors, Elliot Lake, Ontario(Ni-Cu-PGE) + (Uranium – REE’s), Camping Lake, Red Lake, Ontario (gold)

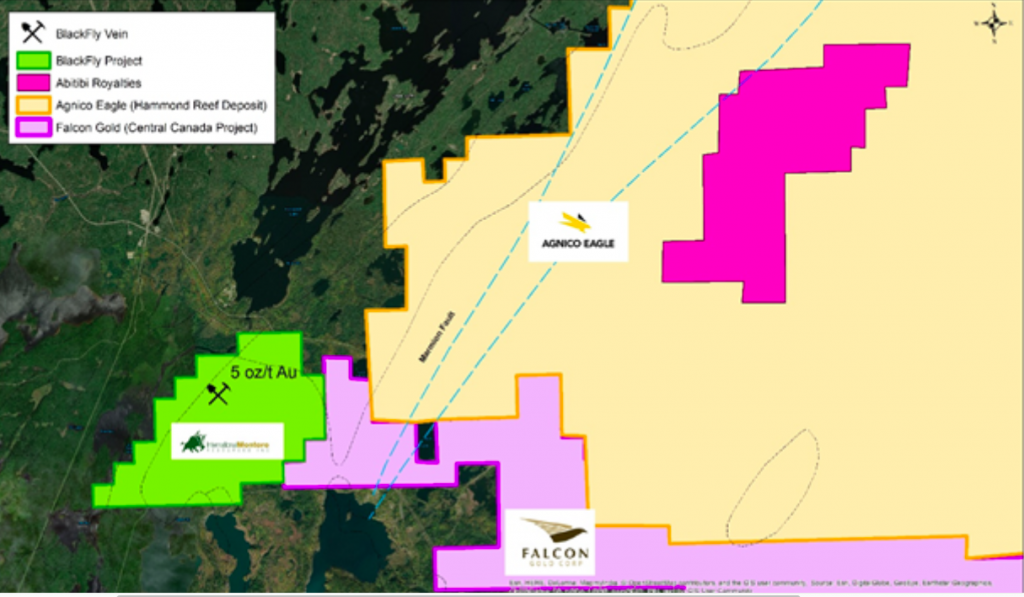

Blackfly property near Atikokan, Ontario

IMT recently entered into an option agreement to acquire the Blackfly Gold property (“BGP“) near Atikokan, Ontario. The BGP claims cover 1,296 hectares. The project is west of Falcon Gold’s Central Canada project, which recently reported 10.2 g/t gold over 3.0 m, and has a non-complaint historic resource of 230k ounces @ 9.9 g/t gold.

NOTE: {Karim Rayani is CEO of both IMT & Falcon Gold, and he’s an active open market buyer of shares in both companies}.

On September 22nd, IMT announced the mobilization of an exploration team for follow-up geological mapping & sampling on the Blackfly Vein. There’s significant mineralization, with values upwards of 15 g/t gold over a 1.1m drill hole interval, and up to 167 g/t in grab samples. The Northwest zone at Blackfly returned drill hole intercepts of 8.3 m @ 0.94 g/t gold and 11.0 g/t over 2.0 m.

Blackfly is ~14 km southwest along strike of Agnico Eagle’s Hammond Reef deposit, which has 4.5M oz. gold. A resurgence of interest in the Atikokan camp is due to development of Hammond Reef and Agnico staking & acquiring surrounding land. On top of Agnico, IMT, Falcon Gold, Abitibi Royalties & Portofino Resources have also secured properties.

Work from 1941 described two gold vein shoots at Blackfly. The southern shoot averaged 11.9 g/t gold over a thickness of 0.33 m on a strike length of 21.6 m. The northern shoot averaged 13.4 g/t over 0.27 m on a strike of 32.0 m. Work conducted by Terra-X in 2010-2012, included compilation of historical reports & data, drilling & surface geochemistry.

TerraX stated in a report that the lineament containing the Blackfly vein has alteration & mineralization traceable over a 4.4 km strike length on the property. The best gold values were from grab samples that graded 167 & 85.6 g/t gold.

Elliot Lake, Ontario (Serpent River/Pecors Ni-Cu-PGE) + (Uranium – REE’s)

X-Terra has been sitting on REE & uranium assets for over a decade. The Serpent River/Pecors property is a 100%-owned, 1,840 hectare parcel in Ontario. Rio Algom mined > 100 million pounds of U308 from similar deposits in the Elliot Lake camp.

A historical, non-NI 43-101 compliant resource estimate of 14.8M pounds (20M tonnes @ 0.037% U3O8) was done. Significant REE values accompany the uranium mineralization. Elliot Lake was a major producer of yttrium as a by-product of uranium production.

This is a nice call option on the uranium price, which has failed to move meaningfully despite the best uranium fundamentals in nearly a decade. Even if uranium prices remain stalled around $30/lb., Serpent River also holds considerable promise for nickel, copper & PGEs like Palladium.

In 2009, IMT commissioned a geophysical specialist to further interpret the airborne survey data. The resulting 3D representation of the inversion block showed an approximate size of 7 x 3 km, and anestimated depth of nearly 2 km, so approaching 40 cubic km….

Everyone knows that gold has soared lately, it’s up +62% since the beginning of 2016. However, few may know that Palladium is up +344%! Think about that, has it been the best performing metal on the planet? Even small amounts of Palladium in the metals mix could be valuable credits to production costs.

Nickel, who cares about nickel? Tesla does! Elon Musk directed a lot of investors towards nickel juniors in comments he made last month, and nickel received additional bullish commentary in today’s Battery Day presentation by Tesla. Nickel looks like an ever clearer winner in Li-ion batteries, while the role other battery metals will pay faces growing uncertainty.

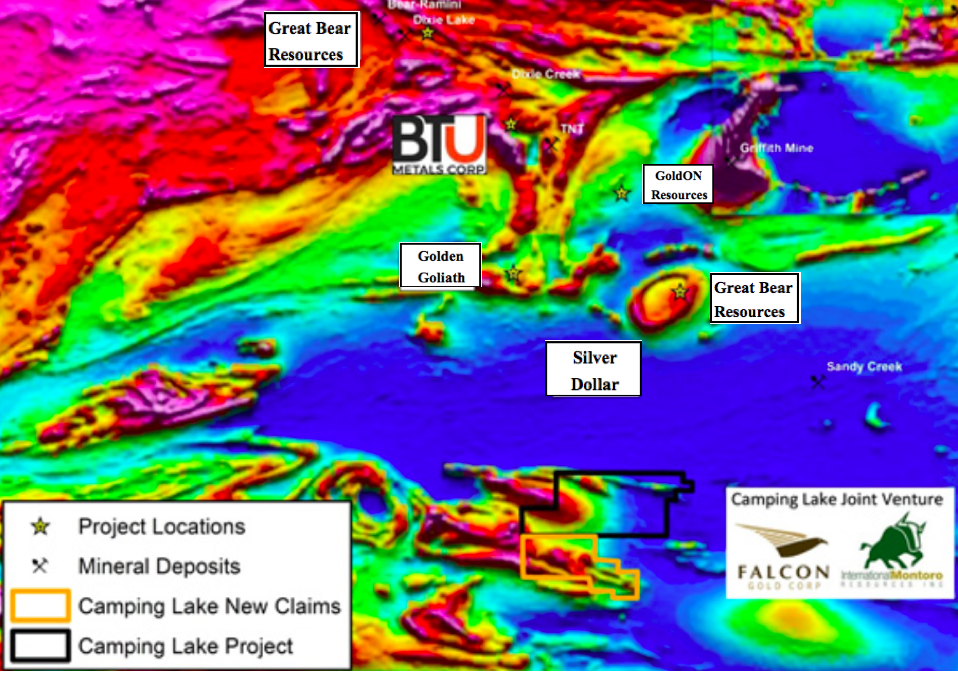

Red Lake, Ontario (Camping Lake – gold)

It’s hard to believe I’m at the bottom of an article about a company with a C$4M EV, talking about a fourth promising property in a well-known jurisdiction. Camping Lake is in the Red Lake mining district of Ontario. IMT is earning into an initial 51% stake in 3,400 hectares at Camping Lake. Falcon Gold is the vendor.

So far, Camping Lake’s main claim to fame is its close proximity to Great Bear Resources’ Dixie project, it’s about 20 km to the south of Dixie. The entire Red Lake district is active with more than a dozen significant drill programs & development activities.

Red Lake’s Pure Gold Mining has surpassed the $1 billion market cap. threshold, up nearly 600% from March. It expects to pour first gold at its high-grade mine in the heart of the district by year end. Pure Gold is widely considered a prime takeout target.

CONCLUSION

A sum-of-the-parts valuation would come up with well north of C$4M. In the hands of larger strategic partners, I think the four assets mentioned herein could be worth 3-4 times the current EV.

In his short time as CEO of IMT, Rayani is doing a great job at drawing attention to the Company. One way is through his ongoing open market purchases of shares, he’s acquired > 1.3 M since the beginning of August.

Could each of the four properties mentioned possibly be worth $3-$5M, on a stand-alone basis, with more eyeballs on each story? Yes. And, valuations on viable mining projects are only headed in one direction. Gold, Palladium, Nickel, Copper, REEs — I truly believe these are some of the best commodities to bet on.

With International Montoro Resources Inc. (TSX-V: IMT) /(OTCQB: IMTFF) /(Frankfurt: O4T1) investors get exposure to a diversified suite of metals. Four projects means four bites at the big discovery apple.

Disclosures: The content of the above article is for information only. Readers fully understand & agree that nothing contained herein, written by Peter Epstein of Epstein Research [ER], (together, [ER]) about International Montoro Resources, including but not limited to, commentary, opinions, views, assumptions, reported facts, calculations, etc., is not to be considered implicit or explicit investment advice. Nothing contained herein is a recommendation or solicitation to buy or sell any security. [ER] is not responsible under any circumstances for investment actions taken by the reader. [ER] has never been, and is not currently, a registered or licensed financial advisor or broker/dealer, investment advisor, stockbroker, professional trader, money manager, compliance or legal officer, and does not perform market making activities. [ER] is not directly employed by any company, group, organization, party or person. The shares of International Montoro Resources are highly speculative, not suitable for all investors. Readers understand & agree that investments in small cap stocks can result in a 100% loss of invested funds. It is assumed & agreed upon by readers that they will consult with their own licensed or registered financial advisors before making investment decisions.

At the time this article was posted, International Montoro Resources was an advertiser on [ER] & Peter Epstein owned shares in the Company.

Readers understand & agree that they must conduct their own due diligence above & beyond reading this article. While the author believes he’s diligent in screening out companies that, for any reasons whatsoever, are unattractive investment opportunities, he cannot guarantee that his efforts will (or have been) successful. [ER] is not responsible for any perceived, or actual, errors including, but not limited to, commentary, opinions, views, assumptions, reported facts & financial calculations, or for the completeness of this article or future content. [ER] is not expected or required to subsequently follow or cover events & news, or write about any particular company or topic. [ER] is not an expert in any company, industry sector or investment topic.